A tool designed for building professionals to help prepare top level cost plans, provide early cost advice to clients and benchmark costs for both commercial and residential buildings

Published: 15/09/2020

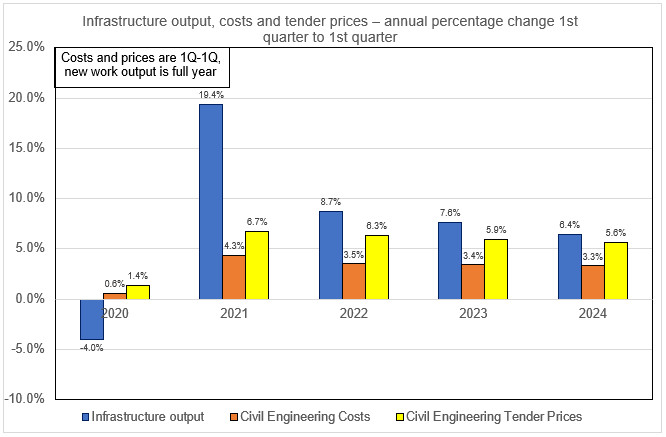

With most work in civil engineering carried out in the open air, and not in confined spaces, the effect of social distancing is proving to have far less downward pressure on productivity than in the remainder of the construction industry. With the Covid-19 led recession and recovery in 2020, civil engineering tender prices are expected to have a moderate rise in the year to 1st quarter 2021 of 1.4%.

Over the following year, with a very sharp increase in output and a return to 100% productivity, the end of the Brexit transitional period, and strong input cost rises, civil engineering tender prices are expected to rise steeply, by 6.7%. Over the remaining years of the forecast period, tender price will be driven by strong output growth, and by input cost pressures, rising by around 6% per annum.

The BCIS central forecast for new infrastructure output shows a relatively small decline in 2020, with a sharp increase in 2021, and then strong but more moderate growth over the remaining three years of the forecast period.

Over the forecast period (1st quarter 2020 to 1st quarter 2025):

- infrastructure construction output will rise by 43%

- costs will rise by 16%

- civil engineering tender prices will rise by 29%

- UK GDP will fall sharply in 2020 as a result of the Covid-19 crisis, with a bounce back in 2021; GDP is then expected to grow by under 3% per annum over the remainder of the forecast period

- the annual general inflation rate is likely to be low in 2020, then rising by around 2% to 3% per annum over the remainder of the forecast period

- interest rates will rise gradually to 1.25% in 2024

- sterling exchange rates will remain depressed for the period of the Brexit negotiations

- the main risks to materials prices will be difficulty in obtaining materials during the Covid-19 crisis, oil prices, tariffs on imports and sterling exchange rates

- nationally agreed wage awards are unlikely to increase over the next year, but will be affected by restrictions in the availability of European labour from 2021.This has been included in the BCIS forecast, but this situation may be mitigated to some extent, by UK construction labour laid off as a result of the Covid-19 crisis, who haven’t been re-employed

- the Covid-19 virus crisis will dampen world demand

- it is assumed that there will not be a significant second wave of Covid-19 and

- the forecast is based on information available up to 11 September 2020.

The Covid-19 crisis has overshadowed the UK leaving the EU but it is still happening. Even though the UK has left the EU with an agreement, there will still be a large number of unknowns to be sorted out during a very short transitional period, ending at the end of 2020.

While almost any outcome is still possible, BCIS will continue to produce forecasts based on three scenarios: a central scenario, an upside scenario and a downside scenario. These reflect the different outcomes from the exit negotiations from the EU and are still equally likely. The uncertainty of the results of the Covid-19 crisis and the Brexit negotiations will undoubtedly lead to BCIS revising its assumptions again as more is known.

In all scenarios, it is assumed that there will be no change of UK government over the forecast period and that there is political stability in the rest of the world. A gradual rise in interest rates puts pressure on consumer spending.

It is assumed that there will not be a significant second wave of Covid-19 in any of the scenarios, and that a vaccine will not be available until some point in 2021.

The full forecast and commentary and the scenario forecasts are published in the Briefing section of BCIS CapX service.

Source: ONS, BCIS