The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance. If you would like to speak with the team call us +44 0330 341 1000, email contactbcis@bcis.co.uk or fill in our demonstration form

Published: 16/07/2026

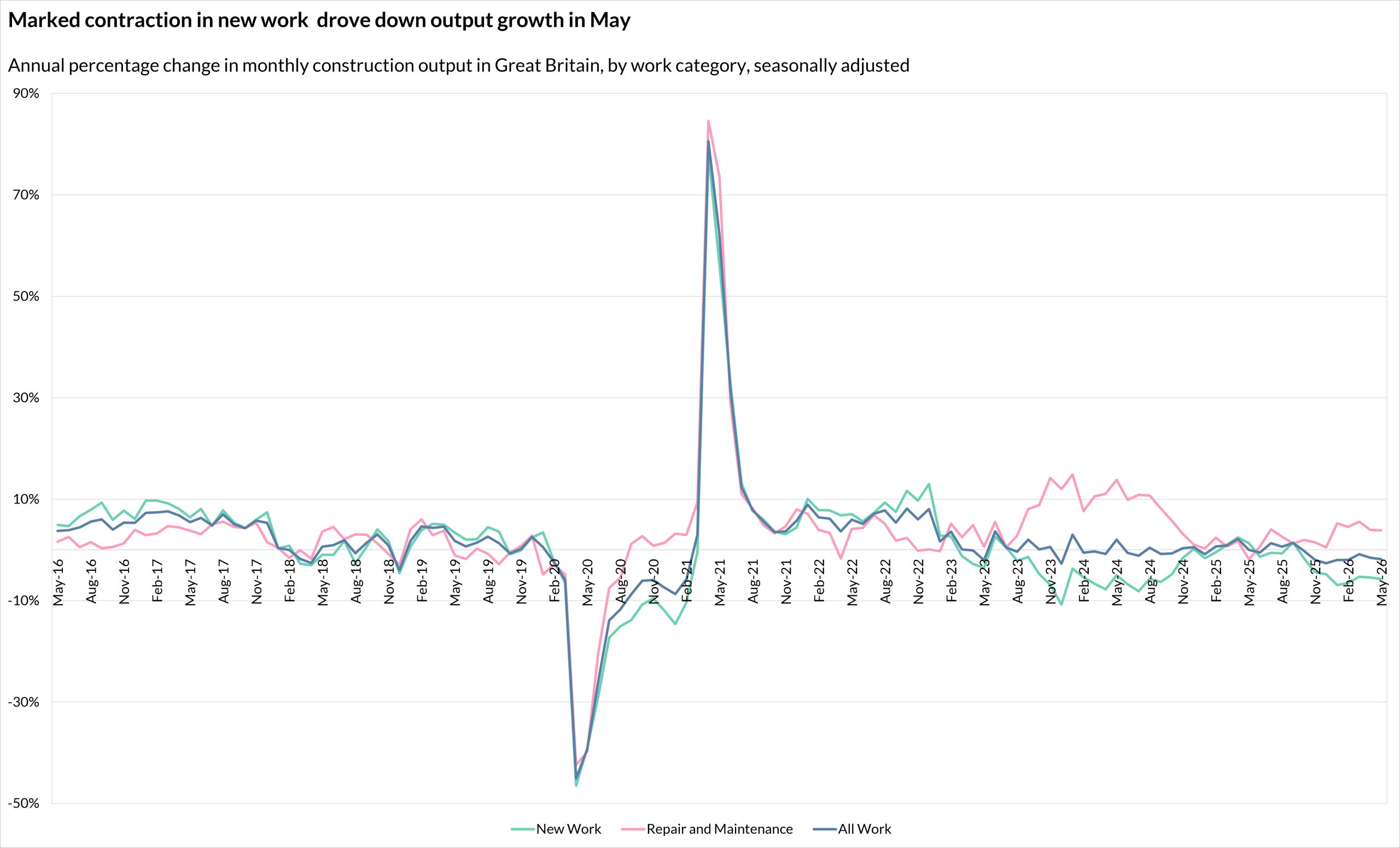

The Office for National Statistics (ONS) publishes monthly estimates of the amount of construction output chargeable to customers for building and civil engineering work in Great Britain, split by sector and type of work(1).

Monthly construction output down in May after R&M contraction

Monthly construction output decreased in May 2026, falling by 0.8% on April 2026, according to the latest ONS data.

New work was up by 0.2% on the month, while repair and maintenance (R&M) fell by 2.1%. The biggest monthly changes were in private housing R&M, down by 5.0%, and public housing R&M, up by 3.8%.

On an annual basis, total construction output fell by 1.8% in May 2026. New work declined by 5.8% compared with May 2025, while repair and maintenance (R&M) output increased by 3.8%. No new work sector recorded annual growth, with output declining across every category compared with the same month last year.

The largest year-on-year decrease was in private industrial work, which saw an 11.3% decline.

In R&M, public housing increased by 2.1% on the year while private housing output rose by 3.6%.

| Sector | Change in May 2026 compared with | |

| April 2026 | May 2025 | |

| New work | ||

| Public housing | -0.1% | -7.3% |

| Private housing | 2.3% | -5.3% |

| Infrastructure | -0.4% | -9.1% |

| Public other | -0.5% | -3.1% |

| Private industrial | -1.9% | -11.3% |

| Private commercial | -1.1% | -0.2% |

| All new work | 0.2% | -5.8% |

| Repair and maintenance | ||

| Public housing | 3.8% | 2.1% |

| Private housing | -5.0% | 3.6% |

| Non-housing | -0.7% | 4.4% |

| All R&M | -2.1% | 3.8% |

| All work | -0.8% | -1.8% |

Source: ONS – Output in the construction industry, Table 2a

Source: ONS – Output in the construction industry, Table 2a

Dr David Crosthwaite, chief economist at BCIS, said: ‘A marked contraction in new work drove the annual fall in construction output in May. Every sector recorded a decline, with the sharpest falls in the private industrial and infrastructure sectors.

‘The latest data suggest confidence in commissioning new construction remains very fragile. Clients and funders are continuing to delay investment decisions amid ongoing geopolitical and domestic uncertainty, and there is a growing sense that this caution will persist until conditions stabilise or projects can no longer be postponed.

‘In the residential sector, recent trading updates from major house builders highlight macroeconomic uncertainty as an ongoing challenge. There is also concern over political uncertainty and the implications for planning, regulation and funding. In response to a difficult operating environment, some developers have reduced land buying and moderated the pace of new site starts.

‘Ultimately, something has to give. With ambitious national delivery targets in place, there is significant pressure on the new government leadership to provide the stability and certainty the industry needs to unlock investment and accelerate delivery. Construction businesses will be looking for clear direction and decisive action in the months ahead.’

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.

(1) Office for National Statistics – Output in the construction industry - here