The Building Cost Information Service (BCIS) is the leading provider of cost and carbon data to the UK built environment. Over 4,000 subscribing consultants, clients and contractors use BCIS products to control costs, manage budgets, mitigate risk and improve project performance

Published: 26/09/2024

From periods of high inflation to thin profit margins and tight cash flow, construction has been vulnerable to insolvencies throughout modern history. But the high levels of insolvencies in recent years – as well as high-profile cases of formerly lucrative firms going bust – demonstrates this is a problem that’s not going away anytime soon.

Rampant inflation

From the pandemic to the invasion of Ukraine and the events that continue to unfold in the Middle East, a series of geopolitical shocks have seen inflation rocket over recent years. And, although it’s rises in the Consumer Price Index (CPI) that tend to make the headlines, BCIS data show that inflation had an even more adverse impact on the construction industry, with some materials experiencing levels of price volatility not seen in a generation.

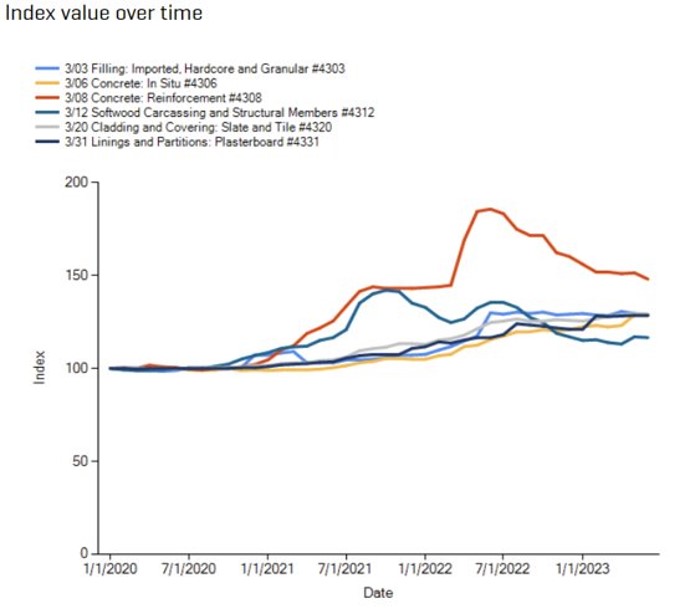

In July 2021, for example, annual growth in the BCIS steel for reinforcement index (Price Adjustment Formulae Indices Series 4 – Civil Engineering and related Specialist Engineering) peaked at 91.8%. Although price increases have cooled for most construction materials, many remain historically high, with structural steel, for example, still higher than pre-pandemic levels. This pressure, coupled with rises in labour and plant costs, has made it increasingly difficult for construction companies to operate profitably or even to survive.

Source: BCIS/ONS

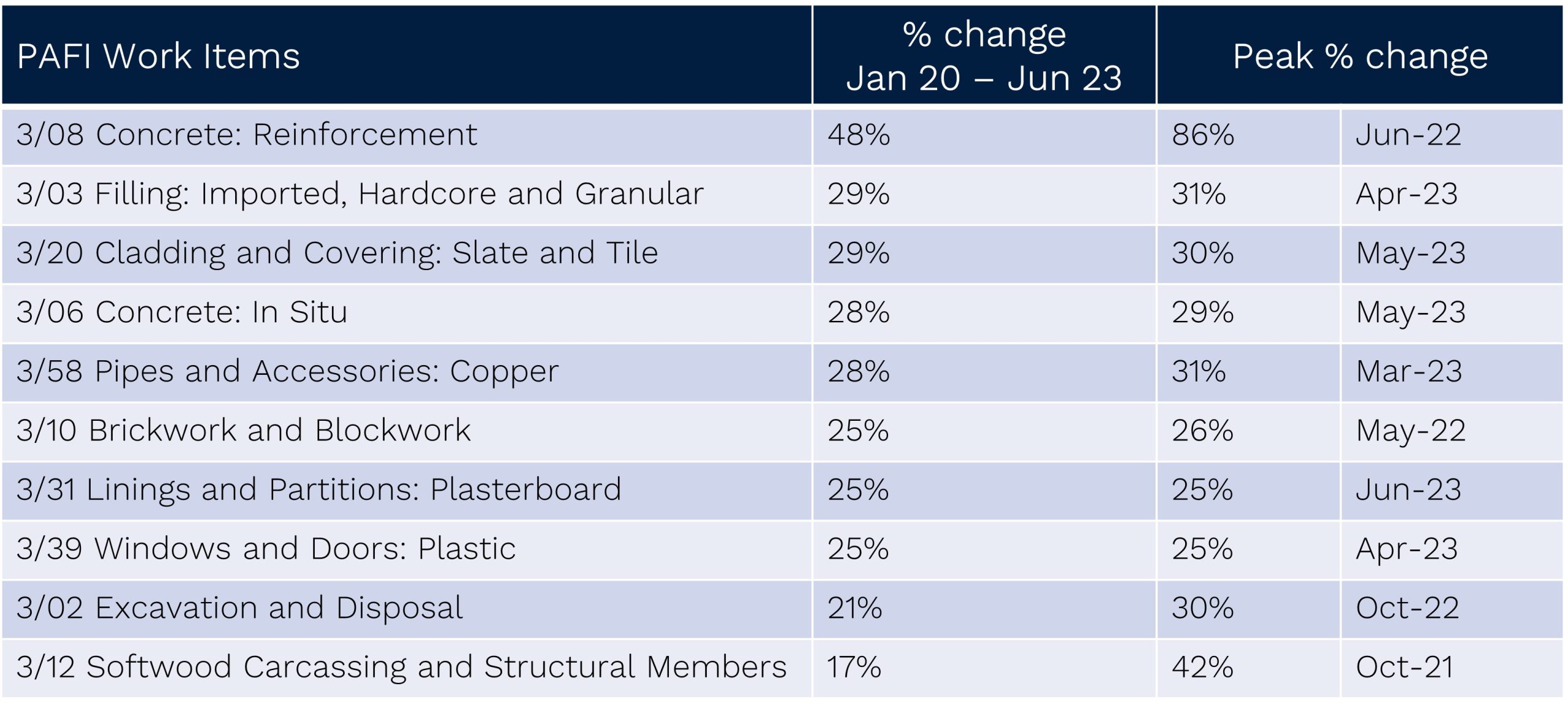

Source: BCIS

High interest rates

The finance that contractors rely on has become much more expensive over recent years due to the base rate remaining elevated.

Aside from construction companies feeling the impact on their own profit margins, it has adversely affected sectors that rely on credit availability. One of the sectors where this has been most evident is the housing market, which, according to EY Parthenon, triggered a fifth of all profit warnings in 2023 – ‘this included housebuilders but also the wider housing value chain, from construction contractors and suppliers to estate agents and mortgage providers’.

In addition, high interest rates create an environment that discourages potential investors or lenders from providing financial support to struggling firms, that could help them recover from financial distress.

Labour as the new cost driver

A report by Currie & Brown – published in June 2023 – claimed an additional 225,000 construction workers will be needed by 2027 to meet demand.

Decreases in new work output, particularly in private housing, have helped to lessen the impact of this shortfall, but labour has become the more significant cost driver for construction, with wages increasing by 6% in the year to November 2024, according to ONS’s Average Weekly Earnings dataset. Although construction pay has been increasing, on average, by less than other sectors in recent months, there has been a determined effort by workers seeking inflation-matching rises.

Among the industry wage awards settled recently, the Building and Allied Trades Joint Industrial Council agreed a 4% increase for builders from June 2024, while the Construction Industry Joint Council agreed on a pay rise of over 4.5% for building and civils operatives. Skilled building and M&E roles have also seen higher growth in pay, no doubt in part because of the knock-on effect of the publicised wage awards for salaried workers.

What does this mean for firms at risk of insolvency? Labour increases tend to squeeze profit margins – firms with salaried staff have the additional expense, regardless of whether they win work or make any profit, while firms who use contract labour will need to pay wages commensurate with inflation.

Exposure to the contract cycle

All the contractors in the supply chain rely heavily on finance and are very sensitive to cash flow disruption. This is because they must pay for materials, labour, and sub-contractors well in advance of payment from their client (ultimate client or contractor). This requires accurate financial planning; a delicate balance that can easily be upset by late payments and fluctuating resource costs.

In addition to this, weakening and uncertainty in demand can be compounded by high finance and political U-turns that make projects unviable or lead to them being cancelled. Typically, contractors in the UK operate at thin profit margins with tight cash flow so they’re especially vulnerable to late payments, a common challenge for contractors in the UK. There have been repeat initiatives and legislation trying to tackle late payment, but it continues to be a problem.

Historically, financially distressed contractors will go to great lengths to keep the conveyor belt of cash moving and, in this economic environment, they must resist the temptation to ‘buy work.’ As tendering becomes increasingly competitive, some contractors may also feel obliged to agree to fixed price contracts, without securing fixed prices from their sub-contractors and suppliers.

However, where contracts do not have an inflation adjustment clause, for example, applying the BCIS Price Adjustment Formulae Indices (PAFI), available in BCIS CapX , it means they have no legal facility to adjust contract sums. This leaves contractors in a particularly vulnerable position if they’re asked to bear the brunt of the rise in labour, materials and subcontractor prices. If the contract extends over a substantial period, any hope of a profit margin could easily be wiped out.

Large and tier-one contractors are also at risk on fixed price contracts, although there has been a move towards more collaborative approaches, to try to avoid the damaging impact of subcontractor and supplier failure.

Subcontractors and suppliers remain squeezed by the impact of cost and labour headwinds, compounded by the slowdown in the housing market.

Conclusion

There are some glimmers of hope amidst the news relating to the high number of insolvencies. The reduction of interest rates, along with the aim to hit Labour’s ambitious housing target of 1.5 million – could help to boost the beleaguered housing market. However, as the dearth of labour skills continue to present challenges for the industry, doubts remain over who will actually build these homes.

And equally, the continuing high numbers of insolvencies in our industry is a huge concern. A reduction in contractors leads to reduced construction capacity, potentially less competition and upward pressure on tender costs. This is a particular issue for sectors and sub-sectors requiring specialist skills, such as M&E, where we may see an increase in demand – especially if the government implements a strategy for decarbonising technologies and retrofits.

Also of concern is the distinct possibility that some contractors will be tempted to under-bid and/or enter into fixed-price contracts that don’t include fluctuation clauses. This will only add to the existing pressures they face, such as late payments, due to the contract cycle. It’s more vital than ever that contractors in the sector continue to focus on running their operations as efficiently as possible, while also mitigating risk for their business and sub-contractors through contracts that contain fluctuation clauses.

Another of our articles that you may find interesting is ‘How can construction cost data reduce the risk of insolvency?‘

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.