If you would like to speak with the team call us +44 0330 341 1000, email contactbcis@bcis.co.uk or fill in our demonstration form

Published: 07/08/2023

In their manifesto in 2019 the UK government set out a housing target of ‘300,000 homes a year by the mid-2020s’.

The figure, which is for England, relates to ‘net additional dwellings’.

Net additional dwellings statistics track changes in the size of dwelling stock due to:

- new builds

- conversions (for example, a house to a number of flats)

- changes of use (for example, a residential house to an office or vice versa)

- demolitions

While the government backed away from this target, they’ve recently recommitted to it, with the emphasis on building in urban areas. There is a view that 300,000 new homes a year would start to make inroads on the affordability of housing, so it is good target for the country.

How many do we build?

In 2021-22 we produced 232,820 net additional dwellings. The average over the last ten years is 178,228, so somewhat short of the 300,000 target.

Approximately 90% of the net additions are new build, so to meet the 300,000 target we need to build 270,000 new homes (houses and flats per year).

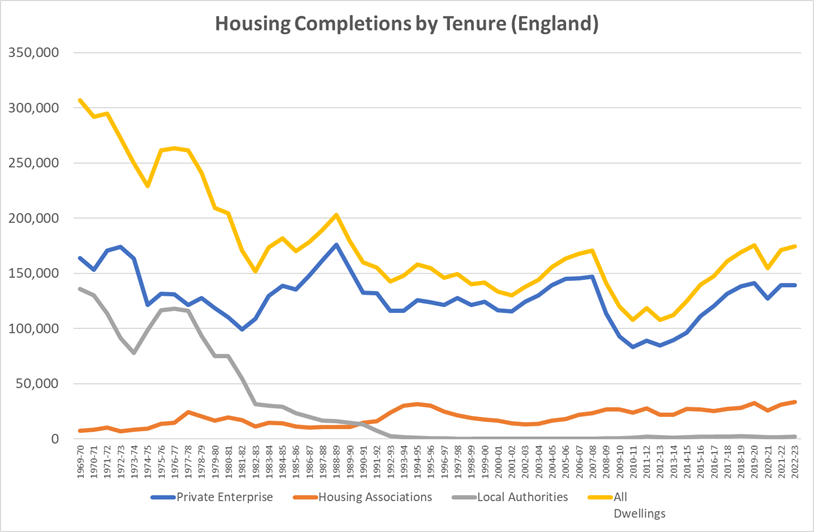

The last time we got anywhere near 270,000i was in the 1970s. Between 1969 and 1973 we built 290,000 per year – for the 70s, over the entire decade, we built 260,000 per year.

Over the last ten years we’ve built about 178,000 per year.

The significant thing about the figures for the 1970s is that while private housebuilders built 55% of the homes, local authorities built 40% and housing associations built 5%.

In the last ten years housebuilders built 81%, local authorities 1% and housing associations 18%. This decline was instigated by ending of the right for local authorities to build houses (see graph below).

The supply from housing associations (registered social landlords) has never replaced the local authority output. This problem was made clear in the Barker Reportii in 2004, which concluded that some form of public investment would be required to drive forward delivery.

The decision to stop local authorities from building, the right to buy policy and denying local authorities the opportunity to re-invest the receipts in housing were political decisions. We’d argue that it’s politics, rather than economics that could help us meet the 300,000 homes a year target.

Where could the houses come from?

As it stands, housebuilders won’t build them all and the public sector can’t build enough.

Housebuilders respond to the market

Housebuilders (developers) will only start a development if they believe that they can sell the houses at a price that returns a development profit. They will only build out a development if there is an actual demand at that price, i.e., they can sell them.

Housebuilders’ share price goes up if they have undeveloped land, it goes down if they have unsold houses. (Not sure that this is logical but that is how the market operates). Therefore, the private sector views housing demand solely as those who can afford to buy the houses that are available at a price that returns a profit. They also build for housing associations but require a contribution to their development profit.

There is a potential demand from those who are actively saving for a deposit for a mortgage or are otherwise in the process of raising funds. Housebuilders would undoubtedly wish to see this potential realised, which is why they’re keen on government initiatives, such as Help to Buy.

Another interesting change in housing delivery is the fall in the number of houses built by smaller contractors. According to the Federation of Master Builders (FMB) ‘Forty years ago SME house builders delivered 40% of our homes. Today the figure is just 12%.’ The factors that have contributed to this decline include the struggle to access finance and land, as well as navigating a complex planning system. Removing these barriers could provide another valuable resource for building new homes.

Can the public sector build enough?

In 1969-70 the public sector built 142,800 dwellings. In 2022-23 it built 35,570 – the highest annual total since the mid 80s.

In 2012, the government agreed that receipts generated by additional sales resulting from the discount increases on right to buy could be used to either: fund replacement stock on a one-for-one basis nationally or allow local authorities to retain their own receipts from additional RTB sales, so that they could reinvest them in new affordable housing themselves. As a result, local authorities have built around 2000 dwellings a year over the past 10 years compared with less than 200 a year in the preceding 10 years.

Housing Association funding is a complex system with many competing factors. They build houses for a range of tenures, social rent, affordable rent, shared ownership and market sale.

Funding for new build affordable housing (social rent and affordable rent) is provided via the Affordable Homes Programme (AHP).

The AHP for 2021-26 is worth £11.5bn and includes a commitment to delivering homes using modern methods of construction (MMC). It plans to deliver up to 180,000 new homes over the next 5 years including:

- 50% of homes at discounted rent, including affordable rent and social rent in areas of high affordability challenge.

- 50% of affordable home ownership including a majority of shared ownership.

Of these:

- 10% of homes to provide supported housing.

- 10% of homes in rural areas.

- 25% of homes delivered through Strategic Partnerships using MMC.

In London, funding is administered by the Greater London Authority, via the £4Bn allocation for their Homes for Londoners programme.

A recent report by the Joseph Rowntree Foundationiii concluded that an additional 700,000 social properties could allow the level of social renting among lower-income families with children to return to its 1979 level. It also concluded that reversing the decline in housing subsidies is key to enhancing the affordability of housing for renters.

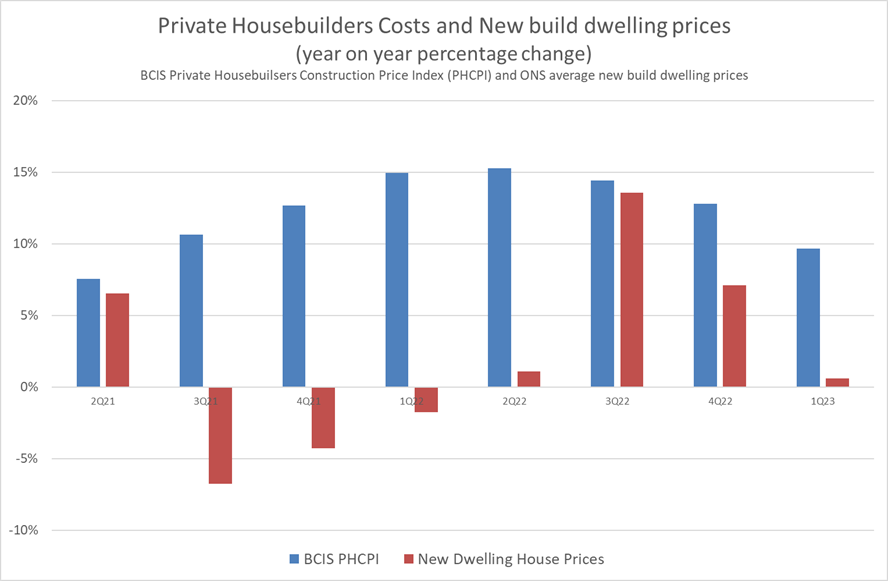

The impact of construction costs on viability

The cost of building dwellings has been rising faster than the sales price over the past two years. This puts the viability of private development schemes at risk.

Source: BCIS & ONS

This will also affect the number of dwellings that housing associations can build on their fixed budgets.

Increasing levels of safety and energy saving regulations will also add to the cost. A recent BCIS survey showed that implementing the recent changes to the Building Regulations – due to come into force in 2025 to ensure homes are ‘net zero’ ready – will add 5% to the cost of construction.

There have been various attempts to reduce the cost of constructing dwellings, not always to good effect, e.g., making them smaller. There have been increases in productivity as new materials have simplified the work in some trades, e.g. plastic pipes for copper for plumbing and the introduction of pre-manufacture components such as door and window sets.

In the main off-site construction such as advanced panel systems and modular construction haven’t been successful. The Government still seems to believe in off-site construction and it may be that a large enough guaranteed pipeline of housebuilding might give off-site construction the market volume it needs but it is unlikely to drastically reduce the cost of building a house.

What can be done?

Given the state of the economy and the housing market, real demand for houses will continue to fall this year. It’s unlikely that it will start to rise until the economy recovers.

To get anywhere near the government housing targets will require political will and government intervention.

- Funding help to buy schemes would boost the demand and supply of houses from the private sector.

- Local authorities could be allowed or, better still, incentivised to start building council houses to meet the need for houses from their population. These could be funded by allowing the authorities to borrow or by building some houses for sale on their developments. Allowing local authorities to identify the demand and the location of the supply may ease planning constraints.

- Government could develop its own land and employ builders to build, rather than selling it to allow developers to develop. Aside from benefiting from the sales, they could use these to produce houses for rent.

Without some form of direct investment, 300,000 homes per year will remain a chimera.

To keep up to date with the latest industry news and insights from BCIS register for our newsletter here.

[i] Note The Department for Levelling Up Housing and Communities (DLHC) publishes an annual release entitled ‘Housing Supply: net additional dwellings’, which is the primary and most comprehensive measure of housing supply.

New build figures from the annual ‘housing supply; net additional dwelllings’ statistical release may not correspond to new build data from the quarterly ‘Housing supply: indicators of supply’ building control reported completions statistical release.

New build data collected for ‘net additions dwellings ‘ is more comprehensive, as collection is over a longer time period, is based on all available evidence (eg site visits, council tax records, planning databases, building control records and any other sources), and may pick up some elements missing from the quarterly new housing statistics (which are based on building control reported completions only).

The quarterly data contains the most up to date figures and is available over a longer time period. Where it was available we have used the annual data.

[ii] Review of Housing Supply- Delivering Stability: Securing our Future Housing Need, March 2004, Kate Barker, HM Treasury on behalf of the Controller of Her Majesty’s Stationery Office.

[iii] Housing affordability since 1979: Determinants and solutions; Ian Mulheirn, James Browne, Christos Tsoukalis; Joseph Rowntree Foundation; January 2023.

![]()