A tool designed for building professionals to help prepare top level cost plans, provide early cost advice to clients and benchmark costs for both commercial and residential buildings

Published: 18/02/2022

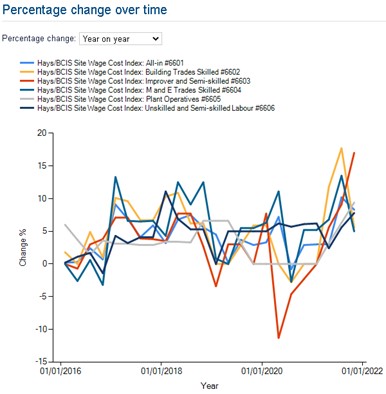

The Hays/BCIS site wage cost indices track changes in the costs of UK construction labour on a quarterly basis. Index values are calculated by BCIS based on data provided by Hays, and represent a measure of trends in the cost of construction site labour for the whole country.

The base data consists of advertised rates for job placements for different labour categories, both PAYE and self-employed. Rates are adjusted to a comparable basis by BCIS before the index values are calculated, representing a consistent measure of costs to the employer.

Significant impacts

Over the period that the indexes were tracked, two of the most significant events to impact them were Brexit and COVID-19. In the months after the 2016 referendum, wages gradually started to rise due to a shortage of skilled labour, and the index rose steadily into 2018.

There was a brief levelling out after this effect had subsided, but in the first half of 2020 the Covid-19 pandemic reduced construction activity reducing the demand for workers and driving the index down.

Since restrictions have eased, there has been a gradual increase in activity which has highlighted a skilled labour shortage. As a result, we can see upward pressure on wages in the index over the last three or four quarters.

Index movements

These indices are published in the middle of the quarter following a period in which data is collected. The data provided by Hays provides an up to date market outlook, giving us a picture of the last quarter.

We can see an increase across the board during 2021 as construction activity recovered from the pandemic in 2020. The labour costs associated with the main building trades rose sharply in 2021. Skilled building trades appear to have dropped back a little in 4Q2021 after they peaked in 3Q2021. The indices suggest strong demand for workers, particularly in the M&E and skilled trades.

Values for individual quarters need to be treated with caution due to a seasonal signal in the rates. They tend to creep up over the course of the year and then level off during the first quarter of the new year, even in the absence of other pressures. So, it is possible that this may still be the case for 2022.

In the most recent quarter; index values for semi-skilled, M&E trades, plant operatives and labourers, have all increased. This is a pattern that is starting to establish itself in the data.

Inflation

A big talking point currently is inflation, as the price of building materials and fuel continues to rise. The latest year-on-year change for the All-In index is 8.3%. While inflationary pressure appears to be global, we are feeling this very keenly in the UK. Some sources and commentators predict this inflation is transitory, while others believe it may be more persistent. It remains to be seen whether strong inflation will exert a continuous effect on the index this year.

Given the present volatility in global markets, forecasts are extremely difficult. Specific forecasts are not provided for the Site Labour Cost Indices, but the anticipated movement in overall construction costs can be seen in the 5-year forecasts for the Tender Price Index (TPI) and the General Building Cost Index (GBCI). Recently the Labour Cost Indices have been rising slightly faster than the TPI or GBCI figures, so the Site Labour Cost Indices need to be viewed within that general context.

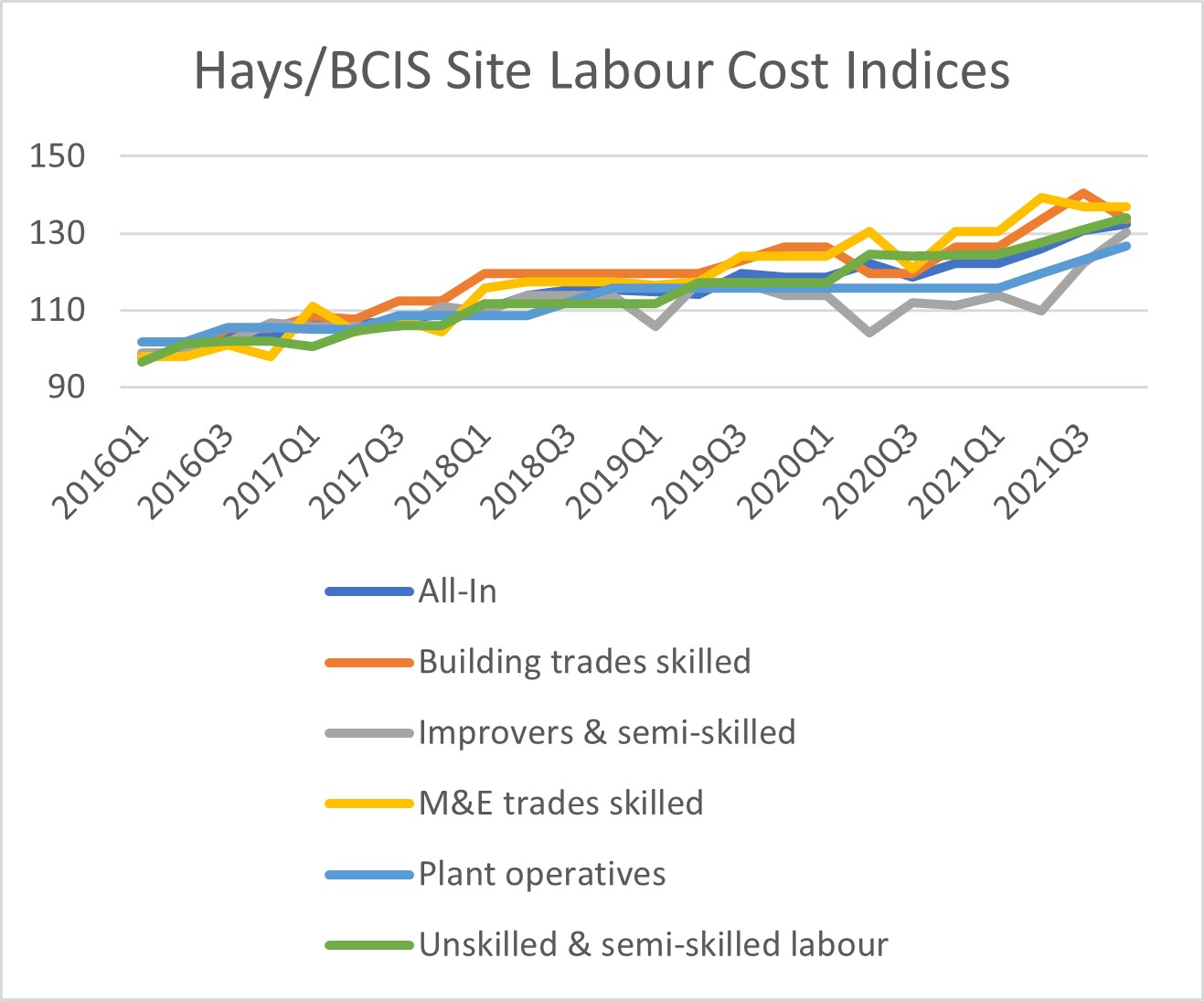

Lower sample sizes in the individual categories mean that the values can be quite volatile quarter-on-quarter. However, the All-In index shows a steady increase in labour costs over the year.

New roles post-COVID?

Over time there has been a fall in the overall sample indicating a decrease in the number of jobs being offered. One effect we are seeing is a larger number of cleaners, sometimes described as “COVID cleaners”, and other job titles such as “COVID Marshall” appearing in the job placements.

These posts are for workers associated with construction and maintenance, who are presumably being employed to maintain COVID precautions on sites. Now that Covid restrictions have largely been lifted, we expect to see these placements reducing in number.

Plant operatives

Last year, after a long period of mostly static wages among plant operators, the Plant index started to creep up in 2Q2021. The year-on-year change for plant operatives in 2020 was 9.4%, ahead of the general trend.

We know from other BCIS research that plant operators generally represent an older contingent within the construction workforce, and anecdotally, that seems to relate to insurance rates for plant operators. It is possible that the shortage of HGV drivers, a persistent issue across Europe and the UK over the last year or so, is driven by the same issues.

Changes in Payroll

We must always bear in mind that the data is obtained from a single source: Hays, and the market is consequently observed from the agency’s perspective. Over time we have seen a fall in the sample size which suggests a decrease in the number of jobs being offered. But this may be a decrease in the number of jobs being offered through agencies and not necessarily a decrease in the jobs being offered to the market.

One of the underlying features of the data analysed by BCIS to create the indices is the proportion of positions offered which are PAYE. It’s interesting to see how that figure has changed. There seems to be some tension between companies wanting to take on employees on a PAYE basis to improve skill retention, and simultaneously not wanting staff sitting furloughed or idle while COVID restrictions are applied. This situation may stabilise now that Covid restrictions are being lifted. The balance of pay types within the sample is changing and the latest ONS labour market overview, UK: February 2022 tends to bear this out.

Speaking on BBC’s More or Less, on February 9th, Tony Wilson, director of the Institute for Employment Studies, noted that the number of self-employed people has dropped by an estimated 700,000 to 800,000 from pre-pandemic levels. Wilson said that one reason for this may be changes to employment due the introduction of IR35, which means that more people are paid through payroll. While more people may be employed on a PAYE basis, the Institute estimates that there are 1m fewer people in the labour pool compared with pre-pandemic levels, which suggests labour shortages may persist for several more quarters.

The Hays/BCIS index series is available now on BCIS CapX.

![]()