BCIS CapX provides a comprehensive, detailed and easy-to-use method of measuring cost movement for building and civil engineering. Widely used in the construction and infrastructure sector to help fairly allocate risk between the client and sub-contractors.

Published: 06/08/2026

Each month the Department for Business and Trade (DBT) publishes a selection of building materials and components data for Great Britain including statistics on bricks and concrete blocks production, deliveries and stocks(1).

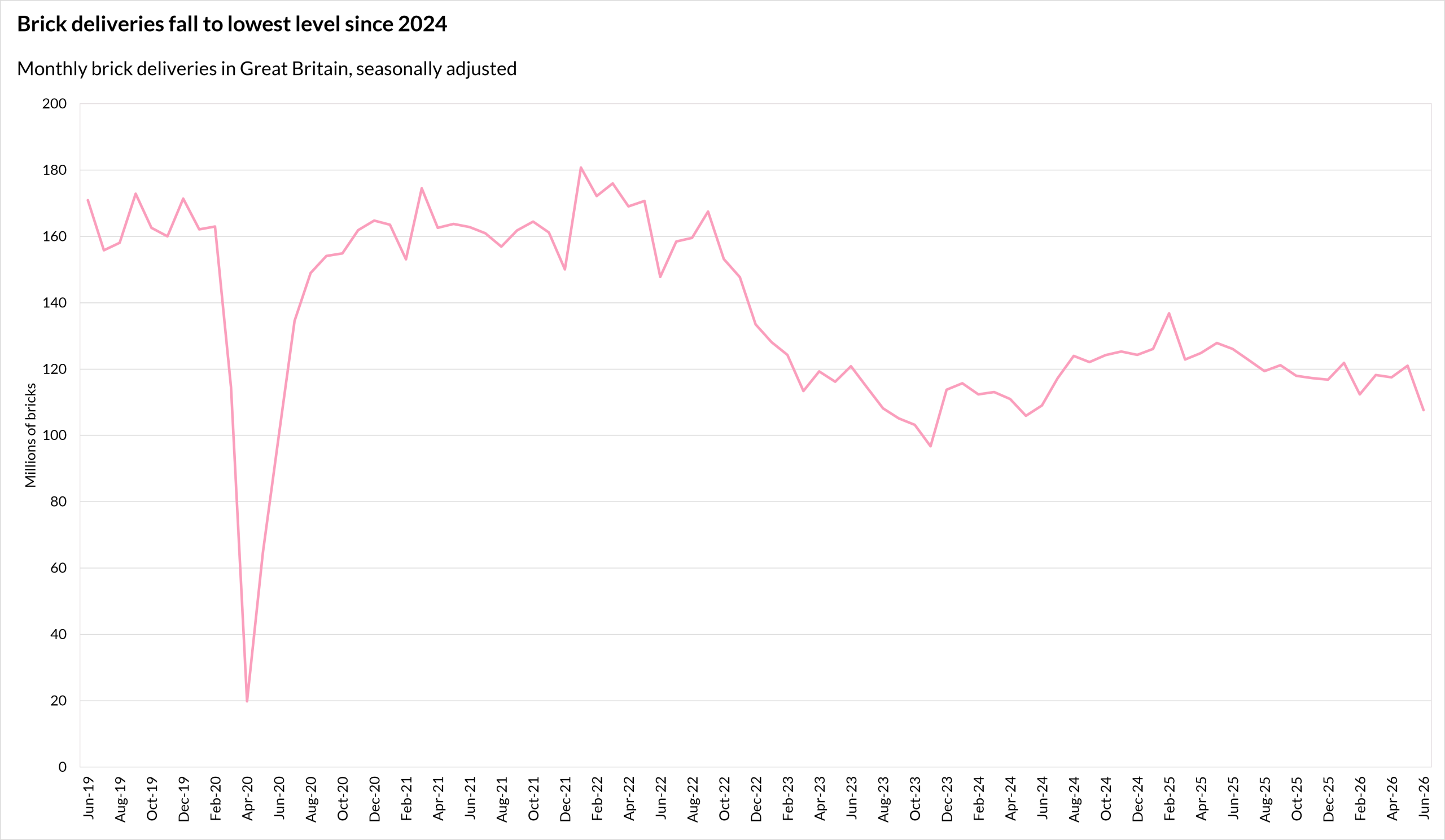

Brick deliveries fall to lowest level since 2024 as concrete block stocks surge

Provisional data published by DBT show brick deliveries (seasonally adjusted) in Great Britain decreased by 16.3% in the 12 months to June 2026, reaching their lowest monthly level since May 2024. Deliveries were also down by 11.1% on the previous month and by 37.0% on the level in pre-pandemic 2019.

Stocks of all types of bricks at the end of June 2026 stood at 547.8 million, an increase of 14.2% on the end of June 2025 (479.8 million) and 46.9% on the level in pre-pandemic June 2019 (372.8 million).

Source: Department for Business and Trade – Building materials and components statistics, Table 9a

DBT’s report also showed concrete block deliveries (seasonally adjusted) in Great Britain were down by 12.3% in the year to June 2026 and by 9.2% on a monthly basis. Compared with June 2019, deliveries were down by 27.9%.

Total stocks of concrete blocks stood at 9.1 million square metres’ worth at the end of June, an increase of 62.8% on June 2025 and 19.7% compared with June 2019.

The data reflects trends observed in a recent trading update from construction product manufacturer Ibstock(2). The company reported that total UK domestic brick market deliveries fell by 8% year on year in the first five months of 2026. Revenue also declined across its clay bricks and concrete divisions.

Looking ahead, Ibstock said trading conditions are expected to remain challenging in the near term, reflecting subdued levels of private housebuilding and repair, maintenance and improvement activity. However, stronger rail infrastructure sales have supported its concrete division and investment at selected concrete sites is expected to improve production in the second half of the year.

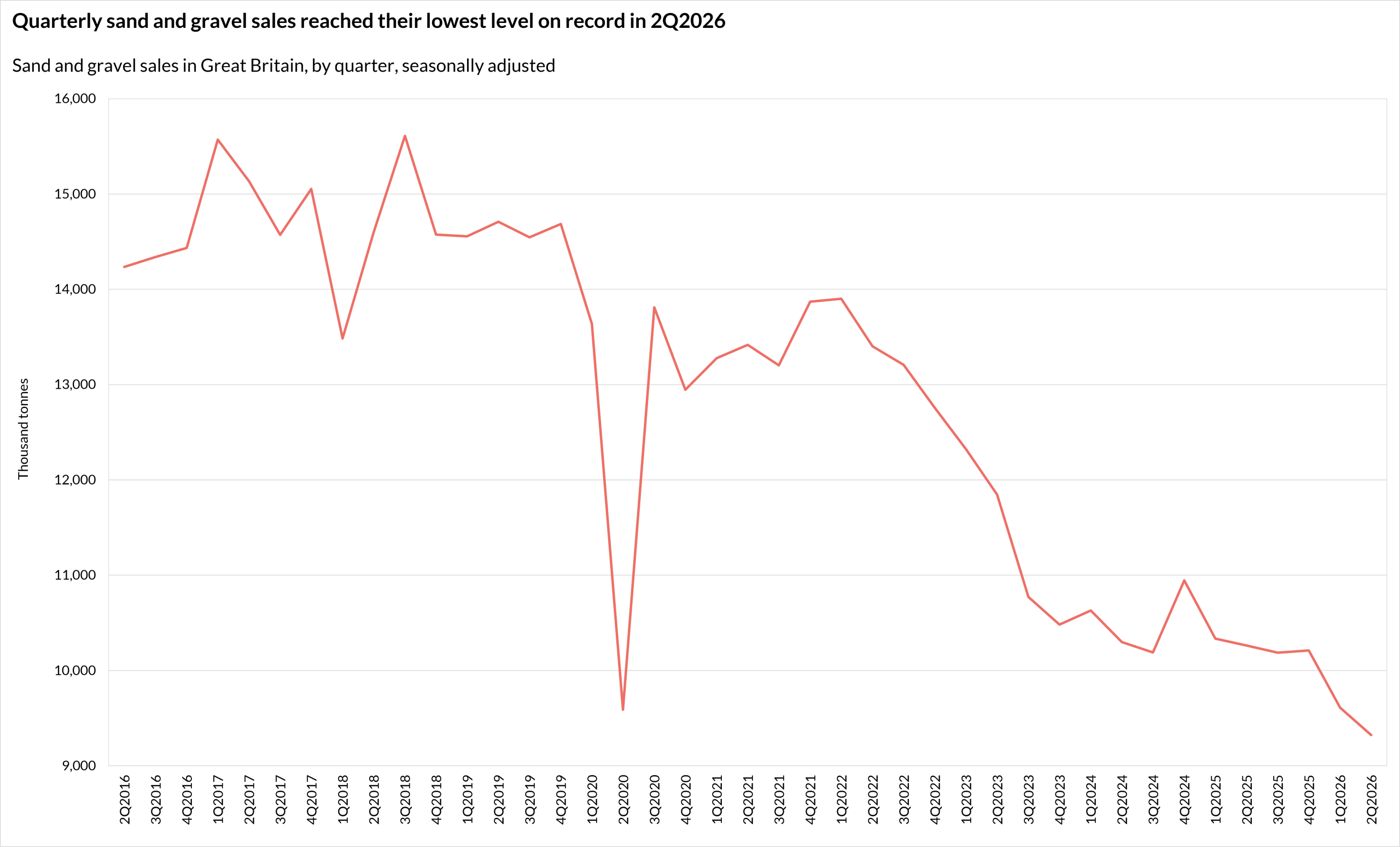

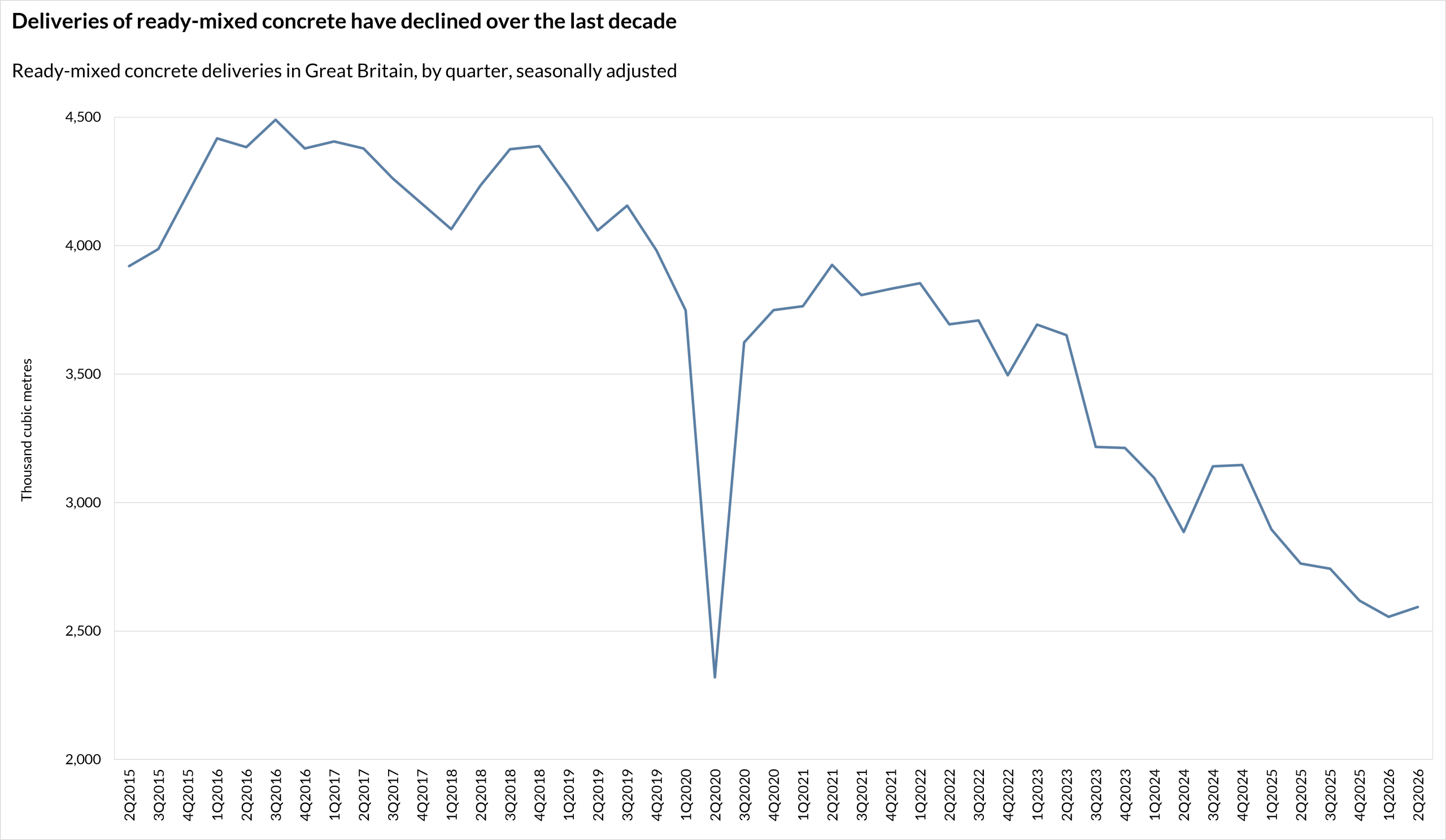

Elsewhere, DBT data going back to 2013 show a longer-term decline in sand and gravel sales and ready-mixed concrete deliveries (both seasonally adjusted).

In 2Q2026, 9.3 million tonnes of sand and gravel were sold in Great Britain, the lowest level shown in the available data and below the previous record seen during the pandemic in 2020. Sales in the second quarter of 2026 were down by 9.2% on the year and by 36.6% compared with pre-pandemic 1Q2019.

Source: Department for Business and Trade – Building materials and components statistics, Table 4a

Meanwhile, seasonally adjusted deliveries of ready-mixed concrete in 2Q2026 (2.6 million cubic metres worth) were down by 6.1% on 2Q2025 and by more than one-third on deliveries in the same quarter in 2019.

Source: Department for Business and Trade – Building materials and components statistics, Table 6a

Dr David Crosthwaite, chief economist at BCIS, said: ‘The latest sales and delivery data from DBT point to a continued and significant slowdown in new construction work, particularly when viewed against historic data. The lowest level of monthly brick deliveries in two years, a 63% annual rise in concrete block stocks and the lowest quarterly level of sand and gravel sales on record are no coincidence. This is what happens when there is too little construction activity to supply.

‘Several factors are contributing to the demand slowdown, most notably reduced client and investor confidence resulting from the conflict in the Middle East and persistent economic uncertainty. Development viability is another major concern. The long-term decline in brick deliveries and aggregate sales can be attributed, at least in part, to developers reining in investment and land purchases as housebuilding costs rise.

‘Month after month, official data tell the same story. These challenges will not disappear overnight, but the government can take further action to incentivise development and stimulate wider construction activity, boosting sales and deliveries of key materials.

‘It is vital that the government considers every available avenue, as there is only so much pressure domestic manufacturers can absorb. The bottom line is that we need these manufacturers if we are to maintain the strength of the construction sector and the wider economy in the years ahead.’

In an open letter ahead of the Autumn Budget, Mineral Products Association (MPA) chief executive Paul Adeleke recently urged Chancellor John Healey to protect capital budgets. He emphasised that, without MPA members, the government would struggle to fulfil its manifesto commitments(3).

New MPA data reinforce the decline in sales of key construction materials, with ready-mixed concrete, aggregates and mortar all reportedly well below last year’s levels.

To keep up to date with the latest industry news and insights from BCIS, register for our newsletter here.